How a Bank-Recommended Technology Fund Cost More — and Delivered Less

A prospective client recently approached us after working with a local bank advisor. At a high level, the portfolio appeared appropriate: a retirement account with exposure to the technology sector and a long-term investment strategy.

However, a closer review revealed a significant issue.

The client had been placed into a commission-based technology mutual fund that carried higher costs, underperformed its benchmarks, and had readily available lower-cost alternatives.

This raises an important question:

Why would an investor be placed in a more expensive investment that delivers worse results?

The Investment in Question

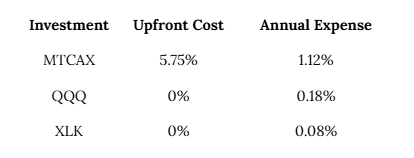

The client was invested in the MFS Technology Fund (MTCAX), which has the following cost structure:

Maximum Sales Charge: 5.75%

Expense Ratio: 1.12%

This means that a meaningful portion of the client’s capital may have been reduced upfront, while ongoing fees continued to compound over time.

MFS Technology Fund (MTCAX) price performance over time.

Performance Comparison

To evaluate the investment, we compared it to two widely used technology benchmarks:

QQQ (Nasdaq-100 ETF)

XLK (Technology Select Sector ETF)

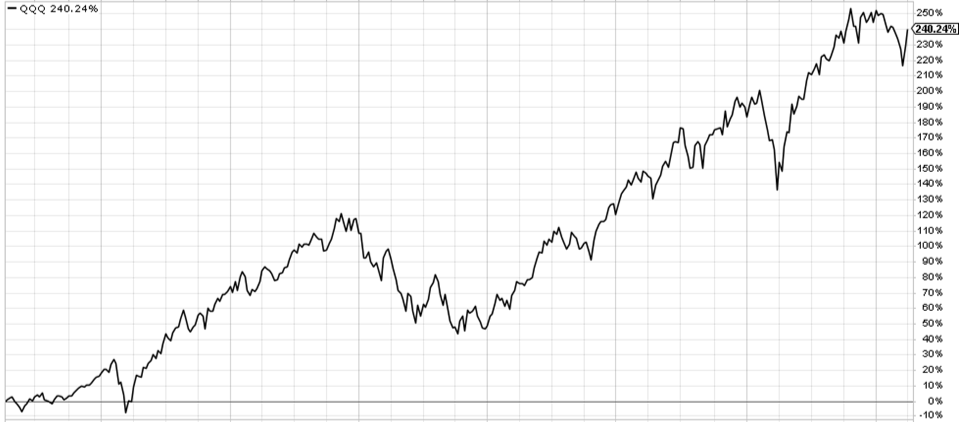

QQQ (Nasdaq-100 ETF) cumulative return.

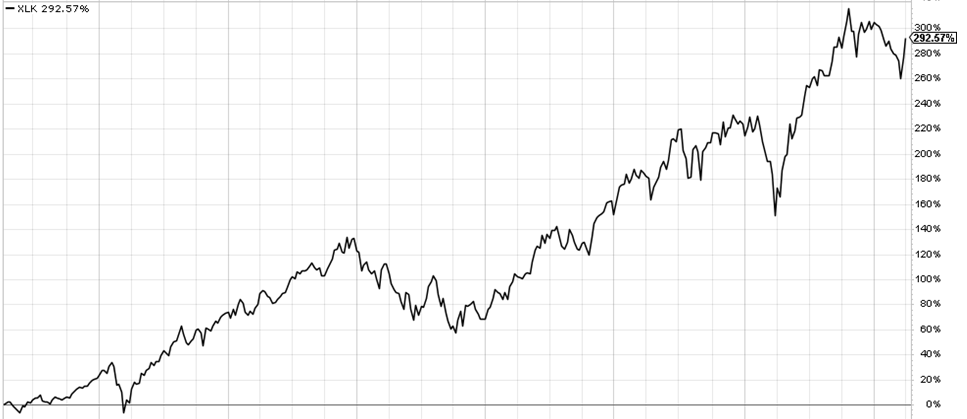

XLK (Technology Select Sector ETF) cumulative return.

Over the same general time period, the results were as follows:

XLK: Approximately 292% cumulative return

QQQ: Approximately 240% cumulative return

MTCAX: Approximately 163% cumulative return

Despite significantly higher costs, the mutual fund materially underperformed both benchmarks.

Now compare that to what the client actually experienced:

MFS Technology Fund (MTCAX) cumulative return over the same period.

Cost Comparison

The difference in cost is not marginal. Over time, these fee disparities can meaningfully reduce long-term portfolio growth.

Understanding the Recommendation

In many bank and brokerage environments, investment recommendations may include products that:

Carry sales charges (loads)

Include ongoing distribution fees (12b-1 fees)

Provide compensation to the advisor or institution

This creates a potential conflict of interest.

While not always the case, certain products may be selected in part because they generate higher revenue for the advisor or firm, rather than because they are the most cost-effective or best-performing option for the client.

The Issue of Transparency

Many investors are unaware of:

The total cost of the investments they own

How fees are structured within mutual funds

How their advisor is compensated

These costs are often embedded and not clearly disclosed in a way that is easy to understand.

Even a 1% difference in annual fees can have a substantial impact on long-term outcomes, particularly in retirement accounts.

Recommended Actions

1. Request Full Fee Disclosure

The client was encouraged to request a detailed breakdown of all fees associated with their accounts, including:

Fund expenses

Sales charges and commissions

12b-1 or distribution fees

Any compensation received by the advisor or firm

2. Evaluate Comparable Alternatives

Investments should be reviewed based on:

Cost efficiency

Performance relative to benchmarks

Transparency of structure

When a higher-cost investment underperforms comparable alternatives, it is reasonable to reassess its role in the portfolio.

3. Consider Account Restructuring

In this case, we evaluated potential account restructuring strategies with the client, including:

Opening an IRA with a low-cost provider

Completing a rollover transfer

Rebuilding the portfolio using low-cost, transparent investment vehicles such as ETFs

These items were reviewed as part of a broader discussion of available retirement plan options, taking into account factors such as fees, investment flexibility, and plan features.

Conclusion

This case highlights a broader issue within parts of the financial services industry.

When an investment:

Costs more

Delivers less

And lacks transparency

It warrants further scrutiny.

Investors should have a clear understanding of both what they are paying and what they are receiving in return.

Final Consideration

Every investor should be able to clearly answer three questions:

What am I paying?

How is my advisor compensated?

How do my investments compare to relevant benchmarks?

If those answers are unclear, it may be time to take a closer look.

This case study is based on a real client experience and is provided to illustrate our advisory process. It is not intended as personalized investment advice or a recommendation, as each client’s situation is unique.